Mortgages, auto loans, bonds and bond funds, home equity lines of credit and credit cards—you may have one, two, or all of them. If so, when have you last checked to see if you have the best interest rates? Chances are that you probably either have not checked your interest rates in a long time, or have never done so because you may not know how. Continue reading to find out what you can do to get the best interest rates on your loans and/or credit cards.

Interest Rate Checkup List

Credit Cards

Do some research on card comparison websites to find the best terms. Whenever the Fed decides to either raise or lower the interest rates, the banks will pass this information onto consumers with variable-rate cards within one or two billing cycles. In addition, take advantage of those promotional offers from banks issuing cards with a low or zero percent interest if your transfer balances from your other credit cards with higher interest rates. Be sure to pay down the transferred balance as soon as you can so that you can limit the amount of interest you will have to pay if the balance is not paid in full.

Mortgages

According to Keith Gumbinger, vice president of mortgage research firm HSH.com, interest rates on mortgages don’t necessarily move in step with Fed policy and have actually decreased following a rate hike last year. Therefore consumers who have excellent credit were able to get interest rates of 3.75 percent or better on 30-year fixed mortgages. He suggests that if you are paying 1 percentage point or more on your current mortgage than what banks are offering, check the numbers to see if refinancing is the best option. He also suggests that if you are close to buying a house, see if you can lock in a rate with your lender as soon as possible because the long-term forecast is for higher rates. Rates have a tendency to rise faster than they fall.

Home Equity Lines of Credit (HELOC)

Interest rates on HELOC’s are typically a combination of the prime rate–what banks charge their best customers–plus an interest margin anywhere from 0-3 percent, depending on the lender. Mr Gumbinger advises people to check that second number when doing research on getting the best deal. If you already have a credit line established, expect to see your interest rate increase after a Fed rate increase. To avoid a bigger monthly payment due to a Fed rate increase, ask your lender to give you a fixed rate on outstanding balances. If you have been a good customer by making your payments on time, the lender just may be willing to help you. You’ll never know if you don’t ask.

Auto Loans

The people who get the best rates for auto loans are those who have the best credit history. People with credit scores of 740 or higher usually get the best rates. Therefore, if your credit score is below 740, (make sure you check your score periodically and before applying for an auto loan) take some time to improve your score. The better your score, the better terms you will be offered the next time you buy.

Savings and CD’s

No matter what happens with interest rates in general, the “pennies” people currently earn on their money in bank savings accounts and CD’s is still in effect. It may take one or two more Fed rate hikes before banks increase their rates. As an alternative, look for banks–especially those that operate only online and credit unions. Currently these institutions have the most competitive rates.

Bonds and Bond Funds

If you own a bond and are holding it until maturity, then the rise and fall of interest rates will not change anything. However, if you want to sell that bond or invest in a bond fund that buys and sells its holdings regularly, a rising rate can have a negative impact. As interest rates go up, the price of older bonds that offer a lower yield decreases. When rates fall, bond prices rise.

According to Sumit Desai, senior fixed-income analyst with Morningstar, you should not avoid bonds if you desire a fixed-income investment. Short-term bond funds are less sensitive to price swings than long-term ones but the yield is lower. Therefore be sure to look at the type of bonds in the bond fund–for example safe government bonds vs. more risky corporate bonds–before deciding whether or not to invest in it. Investing in a bond fund should be made in accordance with your risk comfort level.

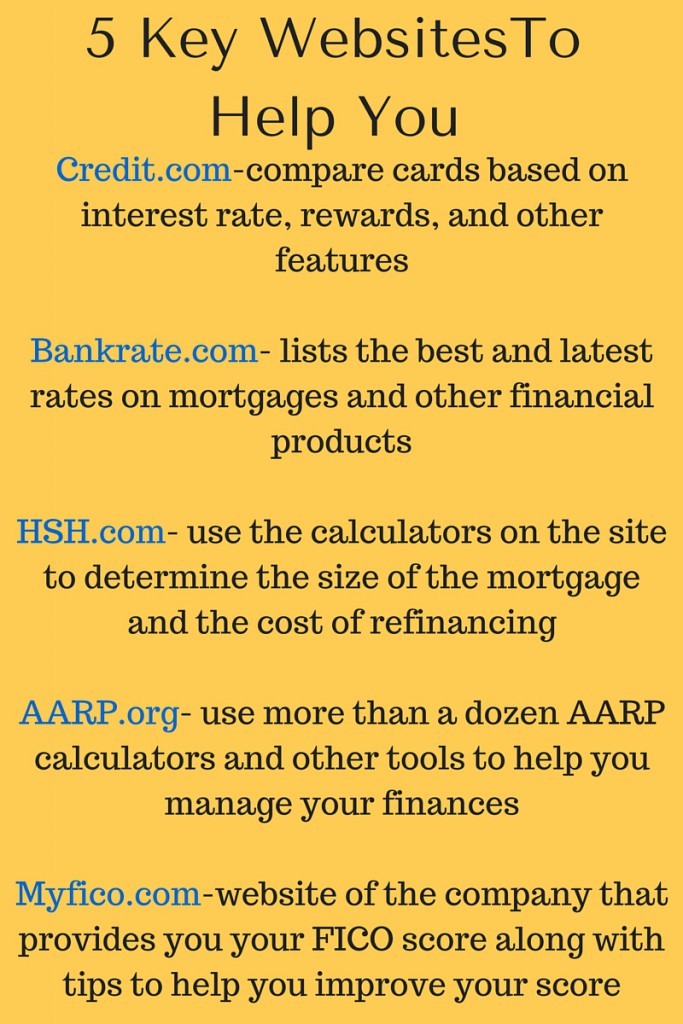

The following websites below will help you in your research for finding the best interest rates.

Hopefully I have given you enough information to get started on checking your interest rates on various financial items so that you are not paying more in interest than you need to. Please feel free to leave any questions or comments below.

Source: “Take an Interest Rate Checkup: Here’s What You Can Do To Get The Best Deals” by Eileen Ambrose. AARP Bulletin/Real Possibilities, March 2016, Vol. 57, No. 2, pg. 4 aarp.org/bulletin

I bought bonds in the Marine Corps back in the 80s. It took 20 years for them to mature at double their initial value. Problem was they didnt compensate for raise in cost of living and the dollar value. While they were a good choice for saving, I wish they paid out what the dollar value of 20 years was. Great post here. As far as credit cards go, I think its important to use them only in emergencies and not to just buy the next gadget you dont have the money for.

Hi Dave,

I think you have hit the nail on the head regarding bonds in that the longer it takes for them to reach maturity, the

less value they are worth. When you cash them out, they only pay in today’s dollars. Bond payouts do not seem to compensate

for inflation. Makes me wonder why people purchase bonds in the first place. You are also correct in your opinion that

credit cards should only be used for emergencies. They make it too easy for people to get in over their heads with credit card

debt. People tend to use credit cards to buy things that they want, not need. Thanks for commenting.