Life insurance–do you think that this is something that is really needed or not? In order to answer that question, you should know what is the purpose of having life insurance, as well as how to decide what type of life insurance is best for you.

What is life insurance?

Life insurance is basically an insurance policy that will replace your income for your family after your death. It basically is supposed to protect your family from financial hardship if you die prematurely. Unfortunately, many people who should have life insurance are either under-insured or do not have any insurance at all. This is not good because if the breadwinner of the family dies unexpectedly, the surviving family members will have a difficult time making ends meet–paying the mortgage, taxes, bills, not to mention funeral costs.

Things to keep in mind when deciding whether or not to buy life insurance

1. Standard of living–can you maintain your current standard of living if your spouse or partner suddenly dies? A life insurance policy can be the difference between maintaining your current standard of living and financial disaster.

2. Long Term Goals–if you die suddenly, your surviving family members may have to take money from their savings to cover burial expenses and other bills if there is no life insurance policy in place.

3. Retirement Income–if the cost of insurance is lowered, this could free up some money that could be used to build up a cash reserve for future use.

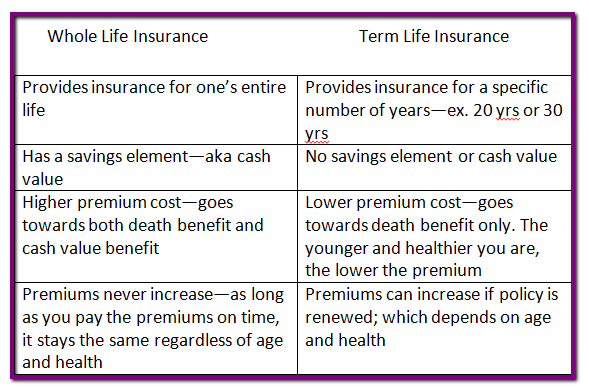

By keeping these points in mind, you can decide which kind of life insurance to buy. There are two main types–whole life and term insurance.

Pros and Cons of Whole Life Insurance

Pros

There several features that whole life insurance has that some people may find beneficial.

- You can borrow funds from the cash value portion of the insurance when you need cash–to pay for medical emergencies, or your child’s education. The interest rate applied to this loan is similar to that of a bank home equity loan.

- Since the premium never changes as long as you pay them on time, the cost of the policy actually gets “cheaper”. Due to inflation, the value of money decreases. This means that the longer you keep your policy, you will actually be paying the premiums with cheaper dollars.

- You have the potential to get tax-free income. When you borrow against the cash value of the whole life policy, that money is not taxed. Depending upon your income tax bracket, the interest paid on that loan can be much lower than what you would pay in taxes. For people who are under 59½ years of age, this can be a way to get early retirement income without having to pay significant taxes and penalties.

Cons

- One disadvantage of having a whole life insurance policy is that the death benefit portion and the cash value portion are not cumulative. For instance, if your policy’s death benefit is $100K and the cash value is $20K, your beneficiaries will only receive $100K, not $120K.

- If you borrowed against the cash value portion of the policy, and the loan has not been repaid before your death, the insurance company will simply deduct what was owed on the cash value from the death benefit; your beneficiaries will only get the remaining funds. Using the same example above, if you borrowed $15K of the $20K cash value portion, and you die before the debt is repaid, the insurance company will deduct $15K(plus interest) from the death benefit. Therefore your beneficiaries would receive $85K ($100K-$15K).

- Loans are not immediately available. On average, the policy must be active with continual payments for at least 5 years. In addition, there is a minimum cash value balance requirement–usually $10K. Both of these conditions must be met before you can borrow money.

Pros and Cons of Term Life Insurance

Pros

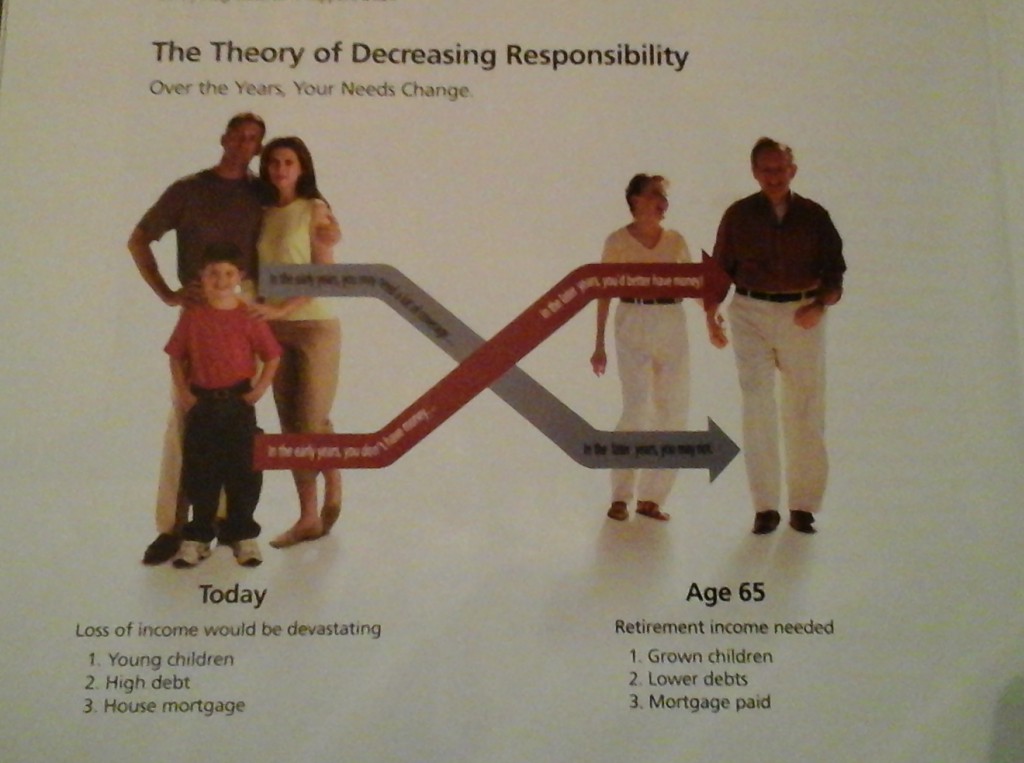

- You will only be paying insurance premiums for a specific term for the purpose of replacing your income if you die prematurely. This is especially important if there are others who depend on your income–children, spouse, elderly parents.

Source: “How Money Works”, Primerica Financial Services, 2001

The general idea is that during your working years when you are young, get married, have children, and buy a house, your income is available to help pay the bills and other related expenses. Term life insurance is supposed to be “just in case”, not permanent. Theoretically, as time goes on, your children grow up, they leave home to go out on their own, and you should have accumulated some retirement income (pension, IRAs or other investments). If this is so, then your need for term life insurance should decrease to the point that it is no longer needed.

Cons

The main disadvantage of term life insurance policies is that the premiums will go up over time because theoretically, as you age, the chances of you becoming ill increase. Also if you let your policy expire or lapse, you may have to pay higher premiums in order to get it reinstated or renewed.

Helpful Tips on Choosing the Right Kind of Insurance Protection

Now that you are aware of some of the pros and cons of whole life and term insurance, here are some quick tips to help you make the right choice:

- Buy adequate coverage. How do you know how much insurance you need? A good rule of thumb is to have 5-8 times your annual salary. This also depends on any other cash assets you may have as well as number of dependents and lifestyle.

- Buy only 1 policy per family. Having several policies will only cost more in processing and administration fees. For instance, instead of having a separate policy for your children, you can have one primary policy with a “rider”.

- Avoid expensive “gimmicks” and insurance policies disguised as something else. Be aware that any extra options offered on insurance policies usually will cost you extra. Make sure that you know what you are paying for. For instance, some insurance companies offer specific types of insurance, such as mortgage insurance. This is not really necessary; if you want your home to be paid for if you die prematurely, just add more coverage to your primary policy. Don’t let the insurance salesperson impress upon you that extra options or policies are necessary; they are not necessary. The one exception to this may be the Waiver of Premium option, which will have your premiums paid in the event that you become disabled for a period of time.

In my opinion, I think term life insurance is the better option rather than whole life insurance. I don’t like the idea of having to pay life insurance premiums for the rest of my life. I’d rather pay for enough insurance that will cover my mortgage and credit card debt and funeral costs while I am still able to work. I also do not like the idea of tying together savings and insurance as with whole life insurance. As I stated earlier, your beneficiaries never get the cash value benefit after you die; the only way to get it is by taking out a loan against it. There are much better ways to build up savings with a higher rate of return than using cash value. Such investment vehicles include self-directed IRA’s , traditional or Roth IRA’s, paper assets, and real estate. You could also create multiple income streams for yourself by either working part time, or starting your own online business.

I can’t stress enough that you should definitely do your due diligence in researching the pros and cons of both whole life and term life insurance. Only you can decide what is best for you and your family. Therefore, once you have completed your research and have decided which type of life insurance to buy, get started today. If you already have a policy in place and want to either make changes or replace that policy, then do so. Timing is everything, and your family’s protection is most important.

Have a great day,

Deidre

Sources:

1. “What Is Whole Life Insurance Explained – Definition & Benefits” by Evan Pierce

2. “How Money Works: Secrets to Financial Success”, Primerica Financial Services, 2001

Thank you for all this information, it has certainly given me some very valuable insight into life insurance policies. I am interested in taking out a policy and I have called a few places for prices.

I was a little put off because a lot of companies just refused to insure me because I am a drug addict and alcoholic. I am 7 years clean but they said they don’t insure addicts.

There was one that said they would insure me but they never came back to me even after I filled out all the paperwork which I found very slack.

Hi Lynne,

It’s unfortunate that you are experiencing a lot of rejection from insurance companies due to your previous drug and alcohol addiction. I guess they think you are too high a risk despite being clean for 7 years (congrats 🙂 However, don’t get discouraged. I did a search and came up with a website page “Addiction Recovery Guide” http://www.addictionrecoveryguide.org where they talked about getting life insurance coverage for former addicts. Another site http://www.termlife2go.com specializes in helping former addicts find life insurance.

Hope this helps. Best wishes for success,

Deidre

The concepts of Term and Whole Life Insurance use to be confusing to me. I have had both so far but currently have Term Life. The price increases are definitely the the biggest draw back. My husband is seven years older than me and our Premiums just had a big increase. I had a few Insurance agents that encouraged me to get Whole Life when I was younger. I didn’t fully understand either at that time. But what I have since learned is that the cash value isn’t really cash, it’s a loan. So even if I don’t have to directly pay it if I die. It still has to be paid back with the policy at death. Even though it may be good for some people in certain circumstances. I can’t see this being the option for me right now. I guess that’s why I have Term.

Hi Karla,

Good for you that you have term insurance and not whole life, because all life insurance is supposed to do is help your family replace your income

(for burial costs and expenses) in case you die prematurely during your working years. You hit the nail on the head when you say that the cash value

part of whole life insurance is really a loan. Also, it is part of the face value of the insurance, not additional insurance. Kudos to you for making the

right choice!

Excellent article. You write very understandable and popular and explain the nature of life insurance. Often this type of writings and other legal documents drawn so as it is hard to understand a nature and nuances of meaning. We have to turn to lawyers which is not a cheap pleasure.

Hi andrejs,

Thanks for the comment. Life insurance is not a topic that most people want to talk about much less understand, so I tried my best to explain the basics of life insurance so that people can understand what it is for and also to help them decide to get it if they need it.

Life insurance is probably one of the best things I’ve bought. When I was younger it didn’t seem to be that important. But when I had my first set of twins, keeping them protected in case something happened to my wife or I, is worth everything!

For how much it costs vs what you get in return if life strikes you hard is awesome! It sucks paying for it every month, but I would cut the cable bill or internet bill before getting rid of my life insurance. You on the same page?

Hi Richard,

Yes, I definitely agree with you. Owning life insurance is one of the most important things you can have if it involves protecting your family in case you die prematurely. I am glad that you realize just how important life insurance is.

This subject always puts a shiver down my spine ( for obvious reasons! ) and I keep on putting it off!

What would be your advice when it comes to choosing a cover – would you research online or would you go straight for the throat and do a face to face ( traditional style? )

Thanks for the article – very informative!

Hi Chris,

Great question… I would do both methods. However, be aware that if you do go to an insurance agent who is in the business of selling either whole life insurance or term insurance, the agent may be partial to the type of insurance that he/she is selling and may try to convince you that what he/she is selling is the best insurance for you. Your best bet would be to first do your research online about each type of insurance and then talk face to face with an agent. This would also give you the opportunity to gather some questions to ask the agent as necessary. Whatever you decide to do, don’t procrastinate–you always want to be prepared just in case.

Hope this helps,

Deidre

Thanks for that, it’s made really clear distinctions between the two.- to be honest I’ve never looked at life insurance, and don’t actually have any. I have to agree with you in that I also think there are many ways of investing our income to ensure peace of mind, and perhaps taking out a life insurance policy is one of these.That is something I would need to look at.

You mentioned creating multiple streams of income, and I would add to that passive income. We have the opportunity nowadays to do just that.

I think that if we invest our money smartly, and of course in ourselves, then that can be part of our life insurance.

Just wondering what the statistics are of people with or without life insurance?

Hi Grant,

Yes you are correct in saying that passive income can also be considered as a way to create multiple streams of income. WA is one way of doing just that. You mentioned that you currently have no life insurance. The important thing to remember is that life insurance is Not for you; it’s for those who are dependent on your income (spouse, kids) in the event if you die unexpectedly. If you are single and/or do not have anyone else dependent on your income, or you have other assets that your surviving loved ones can use to pay off your debts, then you most likely will not need whole life insurance. Personally, I would suggest you get term insurance (it’s cheaper than whole life) but that is completely up to you. Do your due diligence and research before making your decision.

Thanks for reading my post and commenting.

Deidre

Love the Information! I hadn’t thought about getting whole life insurance, currently I have term. I had no clue about the ability for cash advance on these. Im sure rates vary from time and also company, is there a standard amount of time that you typcally would have to pay back the loan? Like 10 years, 5…?

HI Rapheal,

It’s great that you have term insurance already; you do not need to have whole life insurance also. In regards to your question of how long you have to pay back a loan against the cash value of a whole life policy, you do not have to pay it back. It is important to be aware that if the loan is not paid off prior to the policy owner’s death, the insurance company will simply deduct what’s owed on the loan plus interest from the policy death benefit. This means your loved ones will get less money. Thanks for commenting on my post!